The 2016 assessment year goes according to the calendar year, meaning you will be filing your income tax return forms for 1 January 2016 to 31 December 2016. The due dates for submission are as follow:

1. Employers (Form E) by 31 March 2017.

2. Residents and non-residents with non-business income (Form BE and M) by 30 April 2017.

3. Residents and non-residents with business income (Form B and M) is 30 June 2017.

4. Partnerships (Form P) is 30 June 2017.

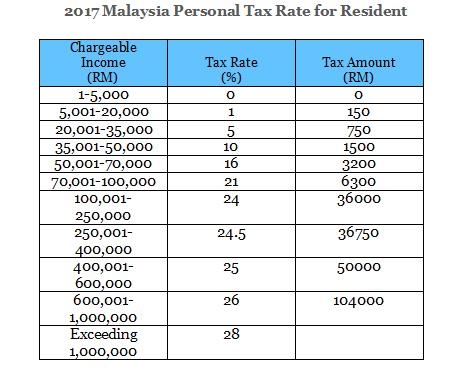

Your payable tax is determined by taking into account your tax rate bracket based on your chargeable or taxable income, which is calculated after tax exemptions and tax reliefs.

Usually, your employer would have already deducted a certain amount from your salary every month under the Monthly Tax Deduction (MTD) / Potongan Cukai Bulanan (PCB) scheme, which goes towards paying your tax for the year on your behalf.

By the end of February, your employer should have issued the EA (private sector) or EC (public sector) Form summarizing your entire year’s gross earnings as well as EPF and relevant tax deductions.

However, employers primarily rely on personal data submitted to Human Resources (HR) – such as your annual salary, marital status, and number of children – to estimate how much tax you will be paying.

Because the deductions do not take into account other tax reliefs you are able to claim, they may have been overpaying tax on your behalf. This is why you should be filing your taxes – to claim back your money.

What you might not be aware of is that you can actually opt to submit Form TP1 to your employers instead of filing your tax returns on March/April every year.

Form TP1 ensures that your employer takes into account relevant rebates and reliefs such as insurance, book purchases, and medical expenses to adjust your MTD accordingly, thus avoiding them from overpaying tax on your behalf.

The TP1 form can be downloaded here.

Have to fulfill the following criteria:

- Such employee must receive their employment income prescribed under Section 13 of the Income Tax Act 1967;

- MTD of such employee must be made under the Income Tax (Deduction from Remuneration) Rules 1994; and

- Such employee must serve under the same employer for a period of 12 months in a calendar year (i.e. Jan 1 to Dec 31).

- This change is effective from year of assessment 2014 meaning employees under MTD as final tax plan who have been submitting their Form TP1 no longer need to submit their tax returns by the deadline next year (i.e. April 30, 2015).